Why Is Your Legacy System Holding You Back (and How to Fix It)

While neobanks launch new products in weeks and payment processors handle millions of real-time transactions seamlessly, companies anchored to outdated infrastructure watch from the sidelines, burning through 75% of their IT budgets just keeping the lights on.

While neobanks launch new products in weeks and payment processors handle millions of real-time transactions seamlessly, companies anchored to outdated infrastructure watch from the sidelines, burning through 75% of their IT budgets just keeping the lights on.

The fintech revolution promised to democratize finance, but there's a dirty secret most companies won't admit: 70% of fintech and financial institutions globally still run on legacy systems built decades ago.

While neobanks can develop and launch new products in just a few weeks and payment processors handle millions of real-time transactions seamlessly, companies anchored to outdated infrastructure watch from the sidelines, burning through 75% of their IT budgets just keeping the lights on.

The cost of standing still has never been higher. Legacy systems aren't just slow; financial institutions lose an average of $93.6 million annually due to limitations, ranging from missed revenue opportunities to compliance failures.

Meanwhile, the gap between what customers expect and what legacy systems can deliver grows wider every quarter. Today's consumers demand instant payments, embedded finance, and AI-powered personalization, while legacy core systems deliver batch processing and overnight updates.

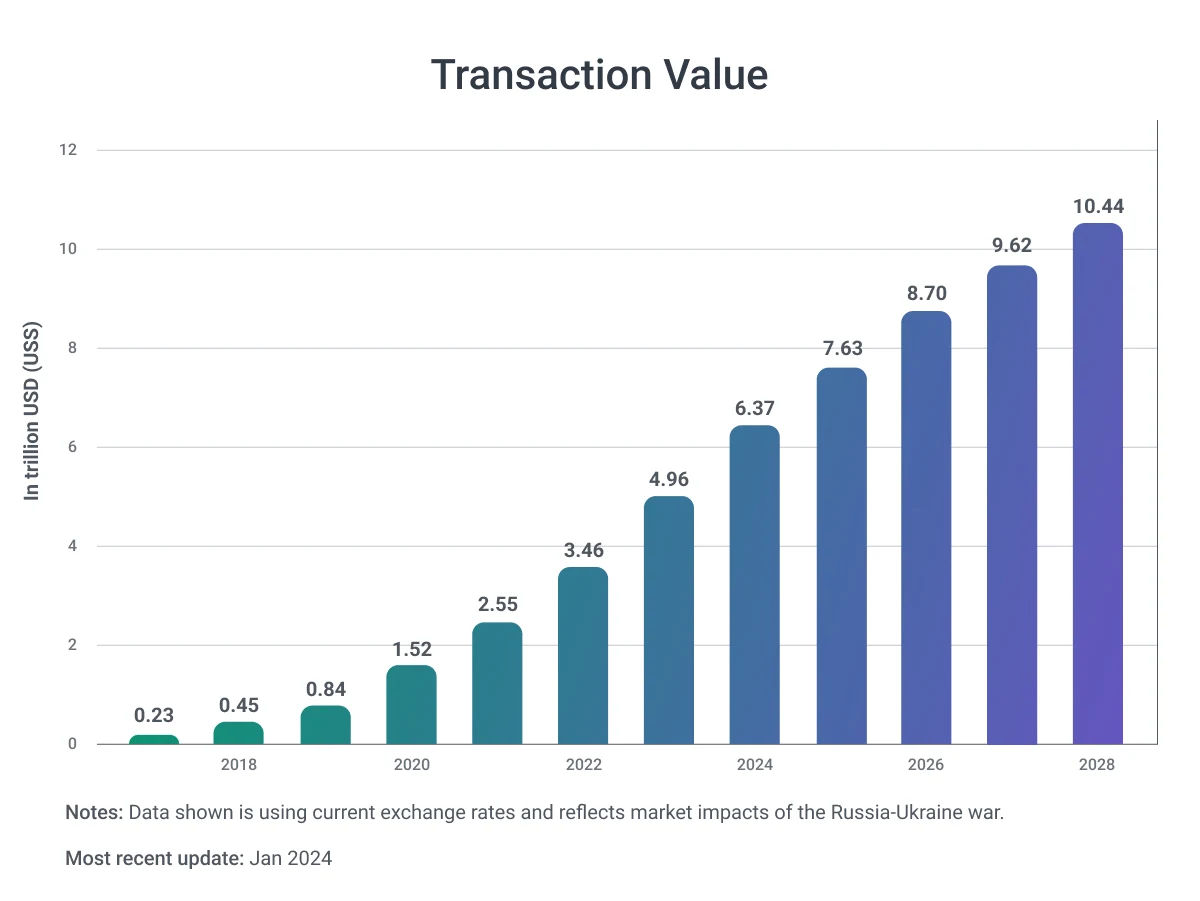

But here's what makes this moment different: the fintech market is exploding from $394 billion in 2025 to a projected $ 1.76 trillion by 2034. Companies that can modernize quickly will most likely capture this growth. The average fintech company running on modern infrastructure launches products three times faster, processes data in real-time, and spends 38-52% less on total cost of ownership than their legacy-bound competitors.

We envisioned this as a practical roadmap for fintech leaders who know they need to modernize but don't know where to start. We'll break down exactly how legacy systems use your resources, often block innovation, and then focus on the proven strategies to modernize without betting the company on a risky "rip and replace" approach.

Whether you're running a payment platform, digital lending service, or embedded finance solution, the path forward is clearer once you understand where to invest and find a reliable partner in the digitization process.

True Cost of Legacy Systems in Fintech

Most fintech CFOs believe they understand the cost of their legacy systems. They see the line items: software licenses, infrastructure maintenance, vendor support contracts.

But these visible expenses represent only a fraction of the actual financial drain. Financial institutions consistently underestimate the true total cost of ownership (TCO) by 70-80%, discovering their actual IT costs run 3.4 times higher than initially budgeted when all factors are considered.

The real cost of legacy systems extends far beyond the IT department. It shows up in lost deals, delayed product launches, customer churn, and the growing gap between your capabilities and your competitors'. Let's break down where the money actually goes and why most companies are shocked when they see the full picture.

The Maintenance Money Pit

IT departments allocate over 55% of their technology budgets just to maintain business operations, while only 19% goes toward developing innovative solutions. For fintech companies, this imbalance is devastating. While you're patching 20-year-old code and babysitting legacy infrastructure, competitors built on modern stacks are shipping AI-powered features and embedded finance products.

The talent costs alone tell a sobering story. The shortage of COBOL programmers compounds as original developers retire, leaving institutions with a shrinking pool of specialists to maintain critical systems. According to recent data, 95% of ATM transactions still depend on COBOL, with 220 billion lines of COBOL code still in operation globally. But who's going to maintain it in five years?

Hidden costs multiply across your organization. Technical debt adds 10-20% to every project cost and manual workarounds replace automated workflows. With custom integrations every vendor update might get broken so what started as a "stable, proven system" can become a high-maintenance liability that consumes resources without driving growth. That's why we advise to first analyze what you have and where you can start updating.

Missed Revenue and Competitive Disadvantage

Here's the painful truth: while you're maintaining legacy systems, you're slowly losing market share.

Traditional banks and fintech companies tied to legacy infrastructure need 6-18 months to bring new products to market, while digital-first competitors accomplish similar launches in 2-3 months. In fintech, that time gap is the difference between capturing a market opportunity and watching someone else get a new product on the market.

The revenue impact is often measurable and quite significant as legacy platforms severely limit your ability to develop personalized products, real-time credit offers, or embedded finance ecosystems that generate new income streams.

Several regional U.S. banks attempted to launch digital-first mortgage platforms but encountered delays exceeding 18 months because their legacy cores couldn't integrate with online underwriting and document management tools. During the same period, fintech competitors launched similar products in under six months, capturing market share that's nearly impossible to regain.

Modern payment infrastructure offers another example. Modern systems integrate with national and international faster payment schemes with relative ease, while companies tied to outdated infrastructures often face delays or must rely on external processors. And relying on external processors can work as a temporary solution, but it's not something a big bank or financial institution can rely on long-term.

The Innovation Tax

Perhaps the most insidious cost is the "innovation tax", the opportunities you can't pursue because your technology won't enable them. Only 32% of financial institutions have successfully integrated AI into their core systems, putting the majority at a significant disadvantage in an AI-driven market.

Legacy systems fragment data across disparate structures, creating silos that prevent the unified customer views essential for modern fintech products.

You can't build sophisticated machine learning models for fraud detection, credit scoring, or personalized recommendations when your data lives in incompatible databases that don't communicate. You can't offer real-time financial insights when your systems process information in overnight batch jobs.

The talent implications compound the problem. Top engineering talent, the people who could actually help you innovate, often avoid legacy technology stacks.

Younger developers and IT professionals are trained in modern software development, cloud infrastructures, and AI systems. Few are willing to build careers around maintaining COBOL or mainframe platforms. This creates a vicious cycle: the older your technology, the harder it becomes to attract innovative minds, which makes modernization even more difficult.

Every quarter you delay modernization, the innovation tax grows. Competitors aren't just moving faster; they're operating in entirely different technological paradigms that enable capabilities your legacy systems can't support at any cost.

How Legacy Systems Obstruct Fintech Innovation

Innovation in fintech isn't about adding features; it's about fundamentally reimagining how financial services work. Real-time payments, embedded finance, AI-powered decision-making, and open banking APIs represent the new baseline, not competitive advantages.

But legacy systems weren't architected for this reality. They were designed for a world of batch processing, closed ecosystems, and predictable transaction patterns.

The Real-Time Payments Problem

Modern consumers expect instant everything: instant account opening, instant loan decisions, instant money movement, while legacy systems were built for overnight batch processing and end-of-day reconciliation.

Legacy banking systems operate on yesterday's information, collecting data throughout the day and processing it overnight, meaning every decision relies on outdated data.

This architectural limitation hits payment companies especially hard. The EU's Instant Payments Regulation mandated that euro area payment service providers be able to receive instant payments as of January 9, 2025, with sending capabilities required by April 2027, often requiring upgrades beyond legacy infrastructure.

Companies scrambling to comply discovered that their decades-old cores simply weren't designed for real-time transaction processing, 24/7 uptime, and millisecond response times.

The business impact extends beyond regulatory compliance. Fintech companies offering instant payment capabilities report significantly higher customer acquisition and retention rates.

But building real-time payment features on top of batch-processing infrastructure is like trying to stream Netflix over a dial-up connection the fundamental technology wasn't designed for it.

Modern systems integrate with national and international faster payment schemes with relative ease, while legacy-dependent companies face costly workarounds that never fully solve the problem.

Embedded Finance: The Integration Nightmare

Embedded finance, the integration of financial services directly into non-financial platforms, is one of fintech's largest growth opportunities.

But it requires something legacy systems fundamentally lack: flexible, modern API infrastructure. Legacy systems often lack the flexibility to integrate seamlessly with modern applications and fintech APIs, resulting in inefficiencies and data inconsistencies.

The problem manifests in multiple ways. Legacy cores typically operate as closed systems with proprietary protocols that resist external integration.

When they do expose APIs, they're often poorly documented, unstable, or require extensive custom middleware. Integrating new technologies with outdated systems can be challenging, with legacy systems often lacking the flexibility to integrate APIs seamlessly with modern applications, leading to data inconsistencies and integration failures.

Modern fintech companies built on API-first architectures can launch new embedded finance partnerships in weeks. Legacy-dependent companies measure the same initiatives in quarters or years, if they can accomplish them at all. Only 32% of banks have successfully integrated AI into their core systems, and similar integration challenges plague attempts to embed financial services into external platforms.

AI and Machine Learning: Stuck in the Past

Artificial intelligence has moved from future promise to present necessity. AI adoption in fintech rose to 88% among top-performing startups, with AI-powered capabilities delivering measurable competitive advantages. AI is expected to save the global financial industry over $500 billion annually by 2030, with a projected $120 billion saved already in 2025.

But deploying AI on legacy infrastructure is extraordinarily difficult.

The architectural barriers are fundamental as modern AI and machine learning require unified, accessible data that can be processed in real-time. Legacy systems trap data in proprietary formats across disconnected databases.

Legacy systems fragment data across disparate structures, creating silos that prevent the unified customer views essential for sophisticated ML models. You can't train fraud detection algorithms when transaction data lives in one system and customer data in another when they don't communicate effectively.

The competitive implications are stark. AI-based fraud detection has reduced financial losses by 40% for major platforms in 2025. AI-powered chatbots now resolve 78% of customer queries without human intervention, dramatically reducing support costs.

Predictive analytics drives 60% of all loan decisions in digital lending platforms. Companies locked into legacy systems can't access these capabilities without serious application integration workarounds that could deliver the same results.

Processing power represents another obstacle. AI workloads require cloud-scale computing resources that legacy on-premise infrastructure can't economically provide. Training sophisticated models demands GPU clusters and elastic compute capacity as legacy mainframes and proprietary servers weren't designed for these workloads.

Open Banking and Compliance: Regulatory Whiplash

Financial regulations evolve quickly, but legacy systems don't. Financial regulations adapt quickly to address emerging threats, with recent requirements focusing heavily on data protection, fraud prevention, and transaction monitoring.

Legacy systems, designed for simpler regulatory environments, struggle to accommodate modern compliance demands.

Open banking mandates present a perfect example. European and UK banks face an increasing regulatory burden, with PSD2, GDPR, and evolving payment security standards creating significant compliance challenges for legacy systems. Research indicates the average bank spends 4.7x more on compliance for legacy systems versus modern alternatives.

The architecture of legacy systems makes compliance inherently harder. Outdated architectures typically lack the granular access controls and detailed audit trails that current regulations require. Implementing proper user privilege management or maintaining comprehensive activity logs demanded by modern frameworks becomes nearly impossible with inflexible legacy cores.

Banks often resort to manual processes and workarounds to achieve compliance, an approach that introduces human error risks while dramatically increasing operational costs. These band-aid solutions never address fundamental architectural limitations that create compliance gaps. Meanwhile, fintechs built on modern, cloud-native platforms embed compliance capabilities directly into their architecture, making regulatory adherence a feature rather than a constant struggle.

The velocity of regulatory change accelerates the problem. Banking is one of the most heavily regulated industries, and legacy systems may not meet current regulatory compliance standards, putting financial institutions at risk of penalties.

Modernization Roadmap: Strategies That Actually Work

The case for modernization is clear. But how do you actually do it without destroying what's currently working? The good news: you don't need a "big bang" replacement that bets the entire company on a risky migration. Modern fintech modernization has evolved beyond the all-or-nothing approaches that failed spectacularly in the past. Today's successful strategies emphasize incremental transformation, de-risking each step while delivering immediate business value.

Understanding Your Modernization Options

Not all modernization approaches work for every situation. The right strategy depends on your specific technical debt, business constraints, risk tolerance, and strategic goals. Legacy system modernization involves deciding between several approaches, each with different cost profiles and risk levels.

Rehosting

Rehosting ("Lift and Shift"): This involves moving applications from on-premises servers to cloud infrastructure without significant architectural changes. Rehosting is a relatively quick, low-risk solution for companies looking to modernize while minimizing disruption. You get immediate benefits like reduced infrastructure costs, better scalability, and elimination of aging hardware, but you don't address the fundamental architectural limitations of your legacy code.

Rehosting works best when you need to quickly exit expensive data centers, improve disaster recovery capabilities, or buy time to plan more comprehensive modernization. But understand the limitations: you're moving old problems to new infrastructure. The system will still be difficult to integrate with modern APIs, still lack real-time capabilities, and still require expensive legacy expertise to maintain.

Refactoring

Refactoring (Rewriting Code): This approach modifies existing code to improve its structure, performance, and maintainability without changing external functionality. Refactoring optimizes applications for cloud environments, improving maintainability and performance. It's more invasive than rehosting but less risky than complete replacement.

Refactoring makes sense when your core business logic remains sound but the implementation has accumulated technical debt. You preserve valuable institutional knowledge embedded in the code while making it compatible with modern development practices. The challenge: it requires deep understanding of both the legacy system and modern architectures, and it's easy to underestimate the complexity.

Replatforming

Replatforming (Moving to New Platforms): Replatforming migrates applications to new platforms or operating systems with minimal code changes. This middle-ground approach updates your technology foundation without requiring complete rewrites. You might move from a legacy database to a modern one, or from proprietary middleware to standard API gateways.

This strategy works well when your application logic is sound but the underlying platform has become a bottleneck. Payment processors, for example, might replatform their transaction processing engines to cloud-native databases that support real-time operations while keeping their core processing logic largely intact.

Reachitecting

Rearchitecting (Microservices Transformation): This represents more fundamental change, breaking monolithic applications into smaller, independent microservices. Microservices architecture enables banks to transform legacy systems into smaller, more manageable components. Each component can be developed, deployed, and scaled independently.

Microservices architecture facilitates easier maintenance, scalability, and flexibility, with each component upgradeable independently, dramatically reducing risk. This approach provides maximum long-term flexibility but requires significant upfront investment and organizational change. It's ideal when you need to continuously innovate and deploy new features rapidly.

Complete Replacement

Complete Replacement: Building entirely new systems from scratch. In some cases, legacy systems are so outdated that the most effective solution is to develop a completely new system. This allows you to design for today's requirements using modern technologies like AI, blockchain, and cloud-native architectures.

Replacement offers a clean slate but carries the highest risk and cost. Implementation can span years and cost millions. Many consider this a last resort, given that implementation can span several years and cost hundreds of millions of dollars, depending on institutional size. Reserve this approach for systems that are truly beyond salvaging, or when regulatory or competitive pressures require capabilities that are impossible to retrofit.

The Hybrid Approach: Best of All Worlds

Smart fintech companies increasingly adopt hybrid strategies that combine multiple approaches. Component-based replacement allows banks to upgrade individual system elements, significantly reducing risk compared to complete overhauls. This "strangler fig" pattern gradually replaces legacy components with modern alternatives while the old system continues operating.

Here's how it works in practice:

- Identify independent components of your monolithic system and modernize them one at a time.

- Start with customer-facing features that deliver immediate value as these create visible improvements that justify continued investment while you tackle more complex backend components.

A digital lending platform might modernize its application intake and decision engine first, building these as modern microservices with APIs. The new components handle all new applications while the legacy system continues processing existing loans.

Over time, as the modern components prove themselves, you migrate more functionality until the legacy system handles only a small, well-understood subset of operations or disappears entirely.

Progressive modernization prioritizes customer-facing improvements first, demonstrating value before tackling deeper infrastructure challenges. This approach builds organizational confidence, generates revenue to fund further modernization, and delivers competitive advantages throughout the transformation rather than only at the end.

API-First Integration: The Bridge Strategy

One of the most effective interim strategies involves wrapping legacy systems with modern API layers. APIs provide standardized access points that enable integration with contemporary applications without complete system replacement. This creates a facade that hides the complexity of legacy systems behind clean, modern interfaces.

Financial institutions can surpass limitations imposed by legacy systems through API integration, which promotes interoperability between systems and allows for seamless data exchange. This enables participation in embedded finance opportunities, partnerships with fintechs, and integration with modern customer channels—all while legacy cores continue operating in the background.

API-first strategies work particularly well for open banking compliance. Rather than rearchitecting entire core banking systems to support PSD2 or similar regulations, institutions create API gateways that translate between modern RESTful interfaces and legacy protocols. Customers and third-party developers interact with clean, documented APIs while the gateway handles the messy translation to mainframe calls or proprietary formats.

The bridge approach isn't permanent—you're still maintaining legacy systems underneath. But it buys time for thoughtful modernization while enabling immediate business capabilities. API wrappers can effectively modernize aging systems by adding modern interfaces over existing technology without disrupting core operations.

Cloud-Native: The Modern Foundation

The destination for most modernization journeys is cloud-native architecture. Unlike simply moving legacy applications to cloud servers (rehosting), true cloud-native platforms leverage microservices architecture and APIs to enable real-time processing with flexible pay-per-use pricing models.

Cloud-native architectures offer compelling advantages for fintech companies:

- Elastic scalability: Handle transaction volume spikes without over-provisioning expensive infrastructure

- Geographic distribution: Serve customers globally with low latency and data localization compliance

- Resilience: Built-in redundancy and disaster recovery capabilities

- Continuous deployment: Ship new features and security patches without downtime

- Cost optimization: Pay only for resources you actually use rather than maintaining peak capacity

Cloud-based solutions enable strategic flexibility and scalability essential for fintech growth. But be careful: not all "cloud" solutions are created equal. Cloud-enabled platforms, essentially retrofitted legacy systems, differ substantially from true cloud-native solutions built specifically for distributed environments. The former may technically "run in the cloud" while retaining monolithic limitations.

Evaluate potential platforms carefully. True cloud-native systems are built on containerized microservices, use managed cloud services for data and infrastructure, implement API-first design principles, and support continuous integration and deployment. These characteristics enable the agility and innovation speed that justify modernization investments.

Getting Started

Understanding modernization strategies is one thing. Actually, beginning the journey is another. Most fintech leaders know they need to modernize, but struggle with the first step. The paralysis often stems from the sheer magnitude of the challenge: how do you start transforming systems that run your entire business? The answer: you start small, strategic, and structured.

.webp)

Step 1: Conduct a Comprehensive System Assessment

Before modernizing anything, you need to understand exactly what you're dealing with.

Your assessment should answer critical questions:

- Technical inventory: What languages, frameworks, and platforms are you running? Which components are end-of-life? What's the age and complexity of your codebase? Where are the documented vulnerabilities?

- Business criticality: Which systems directly impact revenue? What functionality is absolutely mission-critical? Which components cause the most operational pain? Where do customer complaints concentrate?

- Integration mapping: How do systems connect? What data flows where? Which integrations are brittle or breaking frequently? What external dependencies exist?

- Cost analysis: What are you actually spending on maintenance, support, infrastructure, and talent? Financial institutions consistently underestimate TCO by 70-80%, so dig deep into hidden costs like technical debt, manual workarounds, and delayed projects.

- Risk assessment: Security vulnerabilities deserve particular attention, as outdated technology exposes approximately 60% of financial institutions to potential data breaches. Document known vulnerabilities, compliance gaps, and operational risks.

Step 2: Capture Institutional Knowledge Before It Walks Out the Door

Here's a risk that catches companies by surprise: institutional knowledge, including information, experiences, tactics, and skills acquired by employees, becomes critically important during system migrations. Without proper documentation, organizations risk losing up to 75% of knowledge within 24 hours of learning.

The people who built and maintain your legacy systems hold irreplaceable knowledge. They understand why certain decisions were made, how components interact, where the landmines are buried, and which documented behaviors are actually critical versus historical accidents. Start a systematic documentation process immediately:

- Code archaeology: Have experienced developers document complex logic, undocumented APIs, and critical business rules embedded in code. Don't just document what the code does, capture why it does it that way.

- Process documentation: Map out operational procedures, escalation paths, disaster recovery processes, and manual workarounds that keep things running.

- Dependency mapping: Document all integration points, data flows, third-party dependencies, and system interactions. These connections often matter more than the systems themselves.

- Video interviews: Record detailed walkthrough sessions with key personnel explaining complex components. When they retire or leave, you'll have their explanations preserved.

Step 3: Identify and Prioritize Quick Wins

Modernization is a multi-year journey, but you need to show value immediately. Progressive modernization prioritizes customer-facing improvements, demonstrating value before addressing deeper infrastructure challenges. This builds organizational confidence and secures continued funding.

Look for opportunities that deliver maximum business value with minimum risk and complexity:

- Customer pain points: What complaints do you hear most often? Slow account opening? Lack of mobile features? Delayed transaction notifications? These represent opportunities where even incremental improvements create disproportionate satisfaction gains.

- Revenue opportunities: Can you launch a new product line if you modernize specific components? Are partnership opportunities waiting on API capabilities? Would embedded finance integrations open new revenue streams?

- Cost reduction targets: Which manual processes consume the most operational resources? Where are you paying premium prices for legacy expertise? What infrastructure costs could cloud migration eliminate?

- Compliance requirements: Are regulatory deadlines approaching? The EU's Instant Payments Regulation mandated capabilities by specific dates; meeting these requirements can become your first modernization project with clear business justification.

The strategy involves designing your plan to deliver the biggest benefit and greatest opportunity for success early on. This creates momentum. Success breeds support for continued investment, while early wins demonstrate your team's capability to execute.

A payment processor might prioritize building a modern API gateway that enables embedded payment integrations, generating new revenue within months. A digital lender might modernize the application intake and decision engine first, improving conversion rates and customer experience immediately while the legacy loan servicing system continues handling existing accounts.

Step 4: Build Your Transformation Roadmap

With assessment complete, knowledge captured, and quick wins identified, you can build a realistic transformation roadmap. Begin with strategic business planning—gathering requirements, benchmarking against peers, and setting clear, measurable goals.

Your roadmap should be structured in phases, but remain flexible:

Phase 1: Foundation and Quick Wins

- Complete system assessment

- Capture institutional knowledge

- Establish an API gateway or integration layer

- Deliver 1-2 customer-facing improvements

- Set up cloud infrastructure

- Define target architecture

Phase 2: Strategic Component Modernization

- Migrate specific high-value components to microservices

- Modernize data layer and analytics capabilities

- Implement modern security and monitoring

- Launch embedded finance or partnership capabilities

- Begin parallel testing of modernized components

Phase 3: Core Transformation

- Replace or modernize core transaction processing

- Complete migration to cloud-native architecture

- Sunset legacy components no longer needed

- Achieve full compliance with modern standards

- Optimize and refine modernized systems

The specific timeline depends on your scale and complexity. A fintech startup with less legacy debt might move faster. Established institutions with decades of accumulated systems need longer timelines. Phased approaches break migration into manageable test phases that support iterative improvement based on real-world feedback.

Critically, conduct usability testing in parallel with legacy approaches to compare performance. This parallel testing validates improvements while providing fallback options if issues arise. Never cut over to new systems until you've proven they work better than what they're replacing.

Step 5: Secure the Right Expertise and Partnerships

Legacy modernization requires specialized expertise that most organizations don't have in-house. Legacy modernization services require accurate planning and well-orchestrated execution, so you should have absolute confidence in your engineering team or your IT partner.

Consider where you need help:

- Modernization strategy: Consultants who've guided successful transformations can help you avoid common pitfalls and choose optimal approaches for your specific situation.

- Technical execution: Specialized development teams experienced in both legacy systems and modern architectures can accelerate implementation while transferring knowledge to your internal teams.

- Cloud expertise: Cloud-native development requires different skills from traditional IT. Partner with teams that understand containerization, microservices, and cloud-native patterns.

- Security and compliance: Incorporate robust security measures from day one, as secure financial software development requires encryption, access controls, and compliance with regulations like GDPR and PCI DSS.

Collaborating with experienced fintech companies can help you navigate this complex journey and ensure tailored solutions that align with your goals. Look for partners with proven experience in financial services, deep technical expertise in modern architectures, and a track record of successful legacy modernizations.

The Time to Act Is Now

The evidence is overwhelming. Legacy systems aren't just technical debt—they're strategic anchors dragging fintech companies backward while the industry accelerates forward. With the fintech market exploding from $340 billion to $1.15 trillion by 2032, the companies that modernize now will capture growth.

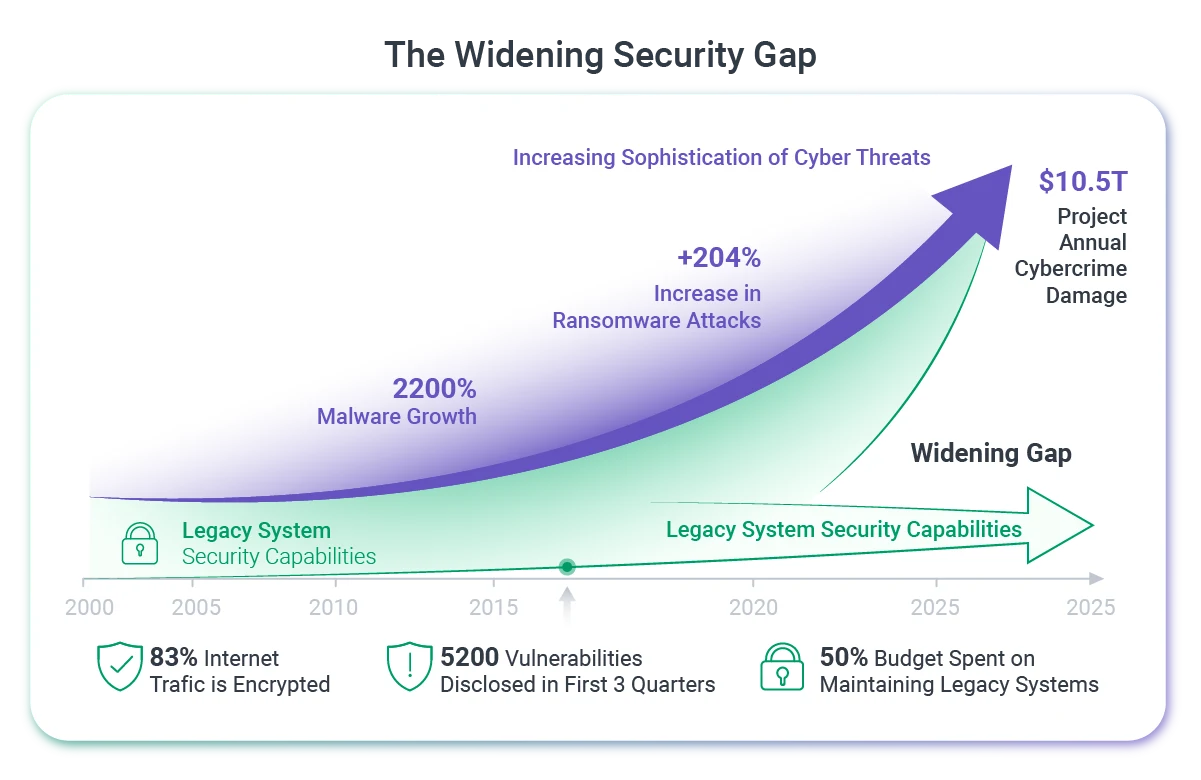

The costs are real and mounting. Financial institutions lose an average of $93.6 million annually to legacy limitations. Banks underestimate true TCO by 70-80%, discovering actual costs run 3.4 times higher than budgeted. Security vulnerabilities multiply as attacks on financial services increase 45% and legacy systems show three times more vulnerabilities than modern alternatives. The talent keeping these systems running is retiring, taking irreplaceable institutional knowledge with them.

The good news: you don't need to bet the company on a risky "big bang" migration. Modernization strategies emphasize incremental transformation that delivers value at every step.

Component-based replacement, API-first integration, and phased migration approaches allow you to modernize without disrupting operations. Start with quick wins that demonstrate value, build momentum with customer-facing improvements, then tackle core infrastructure when you've proven your approach works.

The institutions that successfully modernize gain measurable competitive advantages. Banks that invest in fintech modernization experience 70% enhanced collaboration, 54% acceleration of digital transformation, 56% market expansion, and 55% new customer acquisition.

They reduce operational costs by 38-52%, launch products faster, and build platforms capable of supporting innovation for the next decade. Most importantly, they stop playing defense and start playing offense, defining new categories rather than responding to competitors' moves.

The question isn't whether to modernize 95% of banking executives identify legacy cores as barriers to customer-centric growth, and that number is rising. The question is whether you'll modernize on your own terms or be forced to do it reactively when systems fail, regulations change, or competitors make your offerings obsolete.

The gap between digital leaders and banks hampered by legacy systems is getting wider every day. The challenges, costs, and risks of operating outdated systems will only increase the longer you wait. Companies that act decisively will define fintech's next chapter.

The future of fintech belongs to companies that can innovate continuously, adapt instantly, and deliver experiences that meet rising customer expectations. That future requires modern systems built on cloud-native architectures, powered by AI and machine learning, secured with contemporary protocols, and architected for constant evolution.

Your legacy systems are holding you back. Now you know exactly how to fix it. The only question that matters is: when will you start?