IPC 2021 Takeaways: Traditional Payments vs Fintech? Not Quite

This year's all-virtual Innovative Payments Conference discussed the evolution of payments, better ways to use and handle customer data, and what the future of prepaid might hold

This year's all-virtual Innovative Payments Conference discussed the evolution of payments, better ways to use and handle customer data, and what the future of prepaid might hold

Is it traditional vs fintech? No, at least according to speakers at the Innovative Payments Conference 2021, presented by the Innovative Payments Association (IPA). Instead, traditional payments can be seen as an element of fintech. Industry incumbents have experience, while fintechs can provide a natural evolution for legacy systems.

While the pandemic hit pause on many other industries, finance fared quite well. Transaction volumes were up all around the world. McKinsey research reports that we vaulted forward five years in consumer and business digital adoption in a matter of about eight weeks.1 Tech-driven and tech-enabled businesses were poised to leap ahead but there is still plenty of room for traditional financial institutions (FIs) in the still-evolving financial landscape.

Here we will walk through some of the biggest takeaways from IPC 2021, including the response to the pandemic, how established FIs and fintechs can build the future together, and what aspects of digitization are keeping FIs up at night.

Evolution of Payments

Throughout the conference, payments players advocated for the idea that fintechs were not trying to replace banks, processors, or other traditional FIs. Instead, fintechs are attempting to meet evolving marketplace demands that traditional providers may have been unable to, perhaps due to a lack of technology. Customer segments have unique needs, and want flexible financial instruments to meet those needs.

Consumers Looking for Flexible Financial Products

Although prepaid cards have been traditionally seen as a tool for bringing the unbanked and underbanked into the financial system, that is changing.

"Years ago, the prevailing thought was that prepaid was for people who had no other choice," said Donald Ault, VP of Prepaid Product Management at Comdata. "We've done quite a bit of analysis of our own cardholder base, and we found that more than two-thirds of them or more have active bank accounts. Their annual average income is much greater than one would think, if one were stereotyping what a traditional prepaid cardholder might look like."

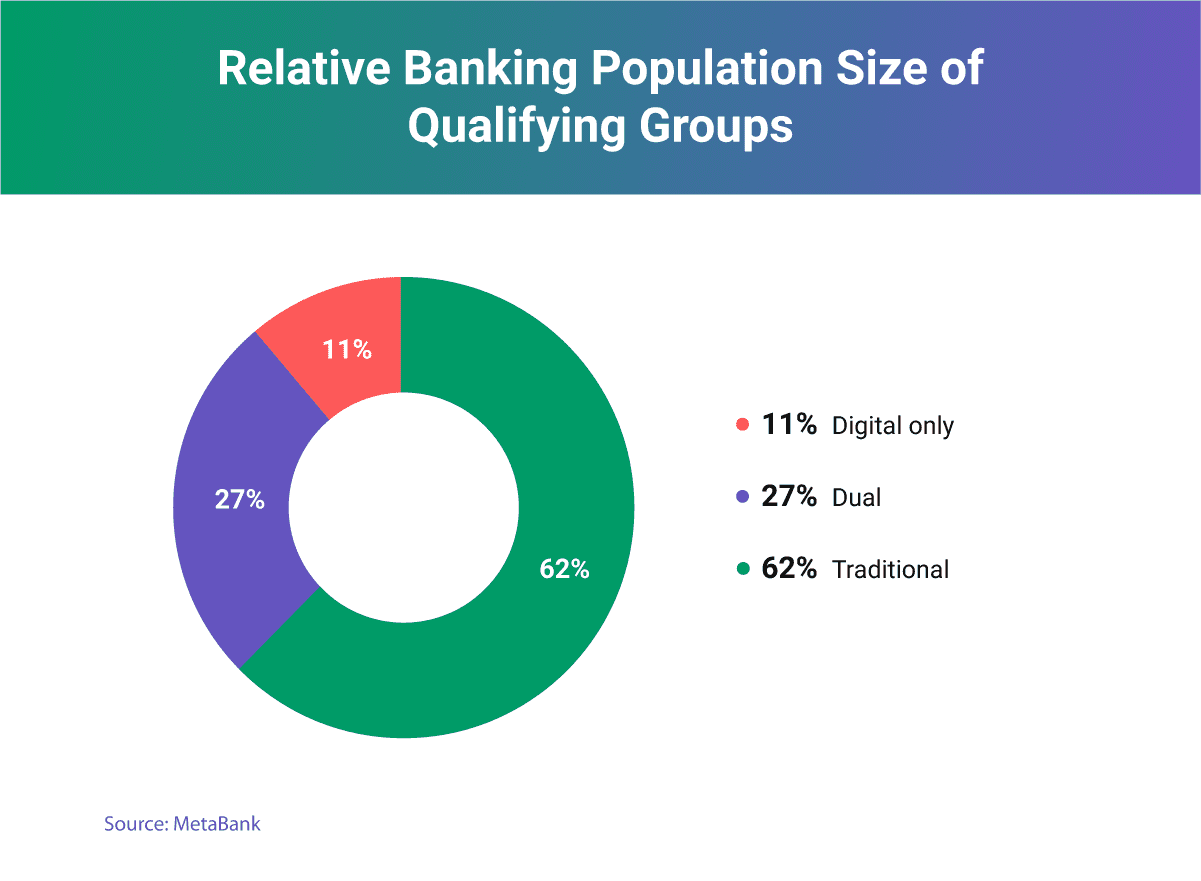

MetaBank reported that while the traditionalist segment is still the largest, 38% of consumers own both a traditional and digital-only banking account. (Credit MetaBank)

Comdata's survey matched findings presented by MetaBank, in that traditional ideas are changing. MetaBank's U.S. study showed that although 62% of bank account holders were traditionalists, meaning holding an account at a brick-and-mortar establishment, a growing number of bank account holders (27%) were hybrid – meaning they held both a traditional, brick-and-mortar account and a digital account. Of the traditionalist 62%, 20% said they were ready to try a digital-only bank account within the next year.

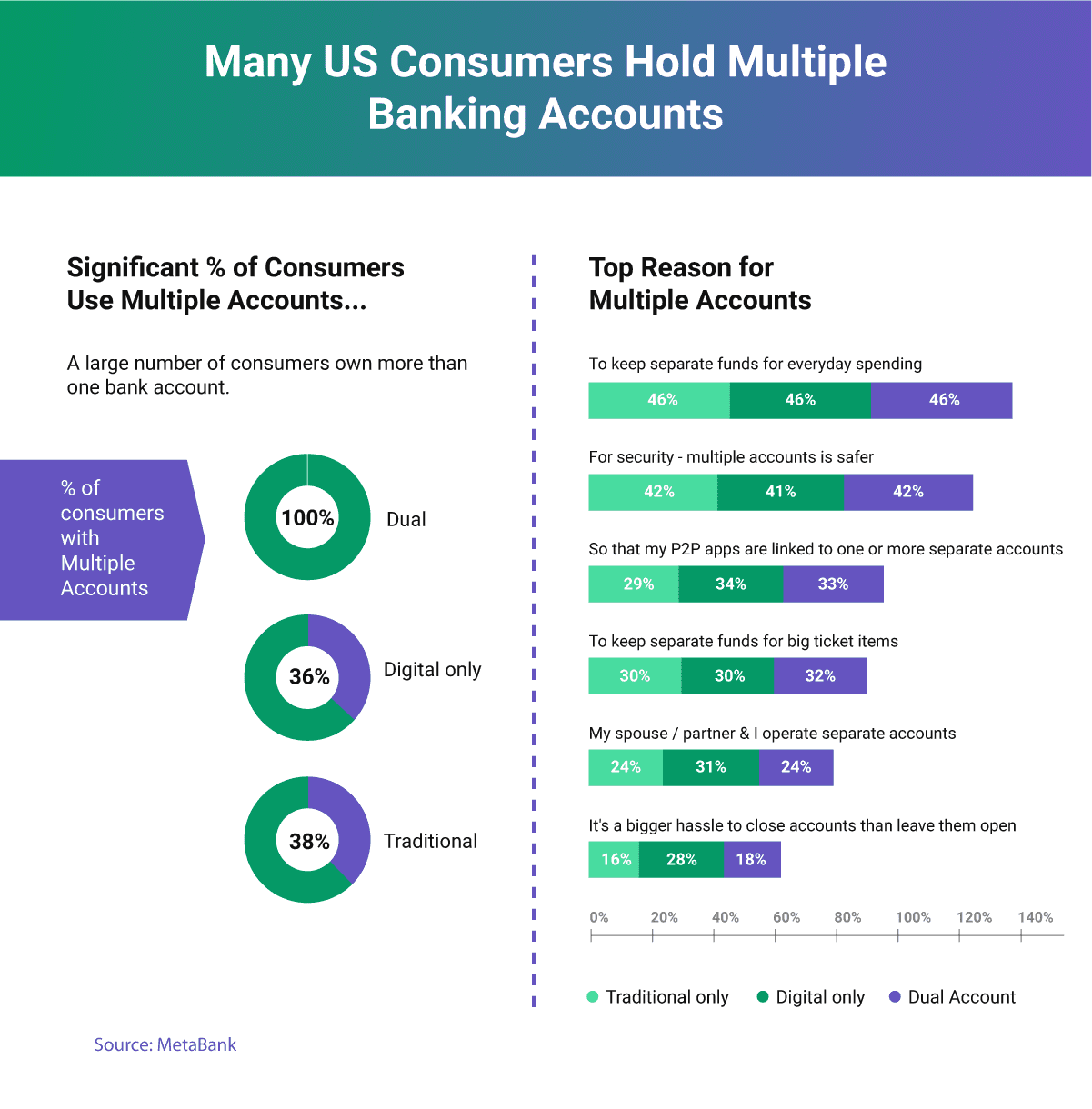

Metabank research showed that a significant percentage of consumers use multiple accounts. Their top three reasons for doing so were budgeting, security, and linking to P2P apps. (Credit MetaBank)

The top three reasons for maintaining multiple bank accounts included budgeting, security, and to provide separate accounts for P2P applications.

Modular Prepaid Fits All Kinds of Use Cases

Prepaid cards are often used in crisis situations, and the pandemic was no different. The U.S. government distributed 4 million prepaid cards during its first wave of Economic Impact Payments (EIP), and then another 8 million during the second wave.2 This was in addition to payments made via direct deposit and check.

Moving forward, financial channels won't be restricted to one or two applications, but be dependent on a consumer or business's specific use case. The focus will be on enabling a flow of funds, whatever form that ultimately takes.

"I think people are about compartmentalizing spending," said Kelley Knutson, President of Netspend, during a panel on Banking as a Service (BaaS). "Operating in different ecosystems, and what they want is value or funds available to transact or collect value within that ecosystem."

BaaS might be something of a buzzword, but it represents a very real shift in the financial landscape. Since 'banking' is part of the term, it highlights how fintechs and established FIs are collaborating to create new services according to customer demands. FIs provide regulatory compliance support, among other specific financial requirements, while fintechs can support legacy infrastructure in getting up to speed in areas such as remote onboarding.

Forward-thinking tech companies, such as Google, are recognizing the power and value of prepaid. Ault gave the example of Google's acquisition of the TxVia platform as evidence that prepaid offers a lot of value.

"I think that speaks to the fact that prepaid can either be a component of a larger fintech solution," he said. "Or it can be used as rails to provide more of a value chain. Prepaid cards have been designed to be modular, so they can easily interact with different issuers, processors, and networks."

Prepaid's Quiet But Enduring Appeal

Another unacknowledged strength of prepaid is its potential for data collection. Collecting and transforming that data into actionable insights is a powerful tool for any business.

"I think one thing that often gets overlooked is how prepaid platforms work," Ault said. "You are keeping track of an enhanced data set. You can keep track of cardholder information. You also have an electronic platform to hold value. It's not just, 'how much money do I have on my card?'"

Prepaid for Data Collection and Customer Analysis

This electronic value can be tied back to a source, enabling traceability that informs a prepaid card provider about shopping habits and preferences. This allows the design of nuanced offerings that meet specific needs. One overarching theme throughout the conference was the need to really nail the customer experience—and there is no better way to do that than with data.

"A lot of [BaaS] players, they don't consider it 'banking,' per se," Knutson said. "They're really about, 'how can I bring specific value to my particular customer who comes into my ecosystem for a very specific purpose based on what it is I'm selling them?'"

Knutson commented that he felt program managers will not be as visible in a BaaS ecosystem, but that provides the benefit of changing their economic model. Those in a direct-to-consumer business are highly dependent on consumer fees and transaction activity. By offering prepaid services behind a fintech curtain, prepaid service providers can tap into different commercial and economic frameworks.

Traditional prepaid card service providers also have the benefit of experience; in providing services to different financial players, whether they are fintechs or not, prepaid card providers can translate how a particular feature could be received by consumers.

"Consumers today increasingly expect real-time transactions," Ault said. "That's leading to more of a focus on the consumer experience. Prepaid makes it easy to do that because it's widely accepted.

"Prepaid makes it easy to sign up for an account, go through all your KYC, receive an account, electronically load funds, all within real time. You can either wait for a plastic card or do all of that immediately."

3 Considerations for Offering Prepaid as a Service

Those interested in providing BaaS needed to focus on a few things, according to experts at the conference: pick a niche, nail it, and do not forget the fundamentals.

"To the question of how [BaaS] providers differentiate themselves, at the end of the day I think it comes down to keeping it simple," said Jenny Johnston, who drives Banking Partnerships at Modern Treasury. "That is really understanding your end customer, whether that be a consumer, whether that be a business, and knowing how to speak their language."

"From a Visa point of view, we spend lots of time and energy focused on things like risk and fraud. I think sometimes it gets a little bit overlooked, because it's not one of the sexy things to focus on," Patrick Williams, Vice President of N.A. Emerging Payment Solutions & Debit Processing Sales at Visa Inc., said. "But I can say, you have a fraud event, and then tell me how your business is doing just after that. So, it is a critical piece [of the BaaS equation]."

Navigating Regulatory Hurdles

Established prepaid card providers also have more experience in designing financial products in a shifting regulatory environment. The pandemic happened to come at a time where regulating bodies were on the precipice of implementing new changes.

"Just as we were designing our new earned wage access product, the [Consumer Finance Protection Bureau] put out some new opinions," Ault said. "We were able to absorb those and design around them. I think prepaid helps to be rather agile in that way, as you're creating new things, you can keep an eye on new regulatory paths that you see and be agile enough to react to them."

The pandemic's acceleration of digital and online payments has likewise pressed down the gas in other areas. Regulatory bodies across the world are looking at how to moderate and create a level field for all interested in playing in the financial sphere, while still protecting consumer interests. All of these changes can potentially impact how fintechs and FIs alike develop and bring new products to market.

Aggressive Regulators in the U.S.?

Payments in the United States are facing a potentially aggressive and skeptical regulatory body as the government shifts from one administration to another. Specific topics touched on during the conference included The Clearing House's letter to the Fed on the Durbin Amendment and the Consumer Finance Protection Bureau's appeal of Judge Leon's ruling on their case against PayPal. The overall sentiment was that increased oversight seemed inevitable.

"I think there's going to be a lot more aggressiveness in terms of perceived improprieties in the market, or perceived breaking of the rules and enforcement, which may lead to other items," said Brian Tate, IPA President & CEO. "My colleague likes to call it the broken taillight theory. I think that's going to be true, eventually, is that once a regulator of any stripe finds a broken taillight, they're allowed to ask you almost any question about whatever it is that you're working on internally."

Shifting Expectations in Europe

The European Commission has new strategies for digital and retail payments that it hopes to unveil soon, but within those strategies, one notable comment was a potential revision of the second Payments Service Directive.

"[The Commission] stated explicitly that they want to cover the whole payments ecosystem, including, for example, technology providers," said Matthias Spangenberg, Senior Consultant at Beust and Coll. and advisor for the German Prepaid Association. "Technology providers not in the flow of funds are currently exempt. The Commission wants to take a fresh look [at the directive]."

Canada Requires More from Prepaid

In Canada, the government has plans to overhaul the whole of its payments regime, including regulations. The government is looking at how to best implement payments modernization, and what regulations will look like within that framework.

This includes a specific AML law that focuses on prepaid cards coming into effect in June of this year. It will place stringent requirements around the issuance of new prepaid cards, ranging from general purpose reloadable to corporate card programs.

The requirements fall on areas such as confirming consumer identity, recordkeeping requirements, PIF requirements, path determination requirements, and much more. Jackie Shinfield, a partner in the law firm of Blake, Cassels, and Graydon in Toronto, Canada, said the requirements will not just affect prepaid cards, but virtual currency as well.

"Depending on the program, it's giving rise to a lot of heartburn," Shinfield said. "There are issuers in Canada who have left the prepaid space [because of this impending regulation]."

Better Ways to Handle (And Use) Data

Improved Business Practices, Better Customer Service

Regulatory oversight is not a new obstacle in the financial industry, but technology can add a layer of complication. With the amount of data generated by people (2,000,000,000,000,000,000 bytes created each day), it quickly becomes confusing as to what data is truly needed by FIs.

Christina Tetreault, Manager of Financial Policy at Consumer Reports, reiterated a line she's said many times: "Is health information financial information?

"Where do the rights begin and why should people care?" she said. "[The open question around data collection] is about helping people make better decisions in their financial lives. That's the real opportunity here."

There is also a strong business case to be made with the idea that less is more in terms of financial data. Tetreault joined Don Cardinal, Managing Director of the Financial Data Exchange (FDX), a nonprofit standards body, in a panel about lessening FIs' use of screen scraping and instead adopting APIs. The movement is similar to Europe's Open Banking initiative.

"There's probably not a more inefficient way of gathering data just from a physical throughput [with screen scraping]," Cardinal said. "An API is an express loading dock. You get your raw materials in a much more organized fashion, much more accurate fashion.

"It's less load for the banks and brokerages because, again, you're not using a bunch of hardware to paint screens for another computer that doesn't care what the other screens look like. It's kind of grown up that way."

With APIs, FIs can gain access to specific information faster, cleaner, and more uniformly. This in turn increases the accuracy of the collected data, which increases security, and increases the actionable benefits of the financial service or product a customer is receiving.

Tetreault said that consumers are increasingly concerned about their financial standing. The panel implied that consumers are looking for services that can give them a realistic financial picture in one location. This means potentially giving companies access to multiple accounts, often with the traditional method of a username and password.

With an API, FIs can instead look solely at the data they need to decide about a product or service, and then release that data once they are done with it.

"You don't hold it; you can't lose it. That dramatically reduces the risk surface in play," said Cardinal. "In cyber parlance, what that means is less things that can go wrong, less stuff to lose."

More Agility in Identifying and Reporting Fraud

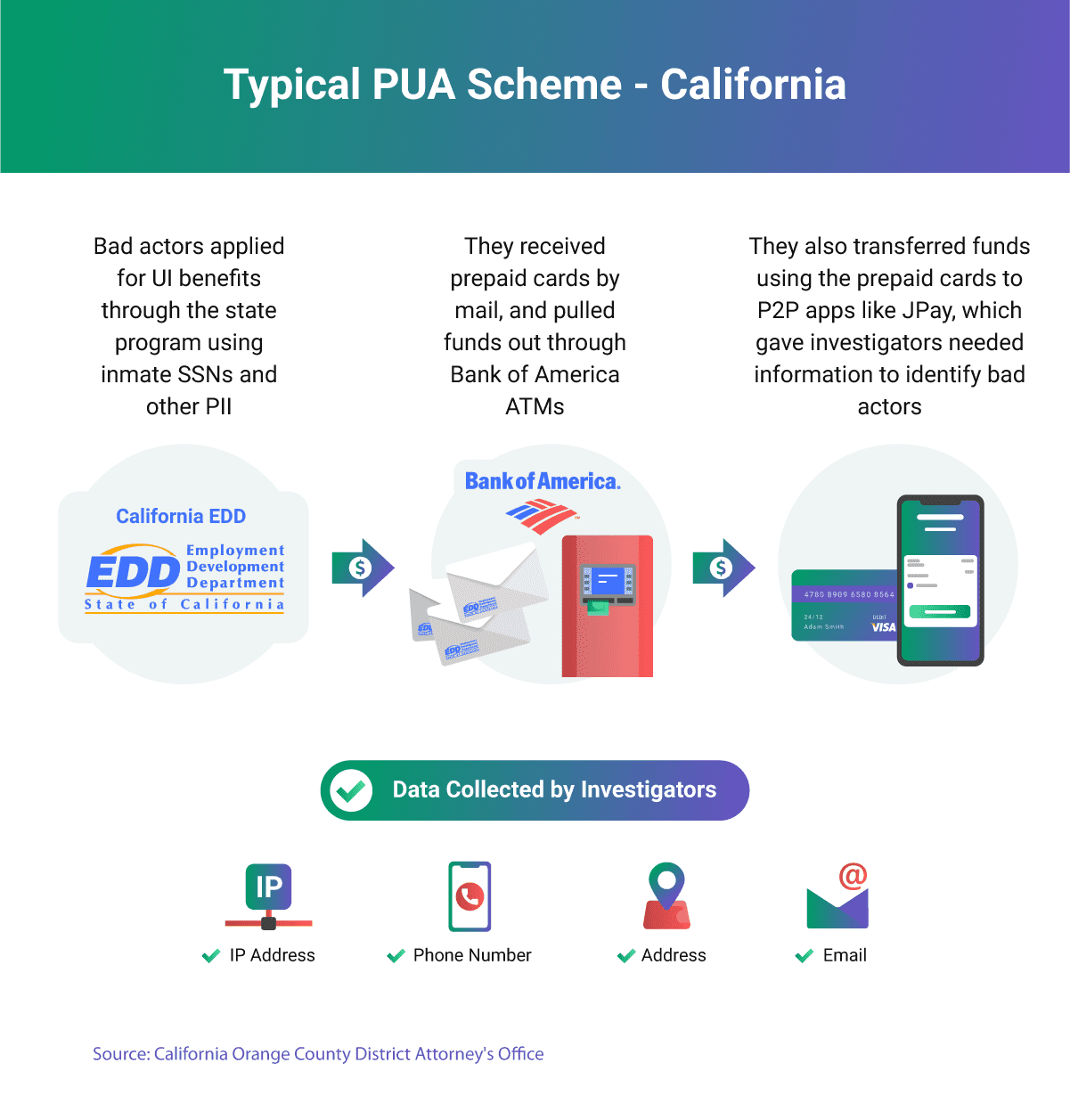

Having insight as to what data an FI has can also impact their ability to mitigate fraud, as well as alert law enforcement to suspicious activity. The CARES Act unleashed a wave of prepaid card fraud in California, where inmates and co-conspirators were linked to the theft of $1B in unemployment aid.3

Using Bank of America ATM footage, Employment Development Department (EDD) prepaid card transference data, and information from peer-to-peer apps, investigators were able to tie together several threads to identify bad actors.

"A lot of people do this using Netspend, PayPal, CashApp, Zelle, GreenDot," Investigator Eric Tapper, of the Orange County District Attorney's Office, said. "The main fintech app that was crucial to our investigation was JPay, a service out of Florida that contracts with 35 states to administer a multifaceted fintech system where you can collect money on books for inmates. You can provide instant message chats, send videos, do it all."

A traditional Pandemic Unemployment Assistance (PUA) scheme involved a fraudulent application, and then transference of funds using an ATM. (Credit Orange County District Attorney's Office)

Tapper emphasized that fintech apps are used for all sorts of fraud, and that understanding which apps collected what information was important to current and future investigations. He added that that information could buttress a Suspicious Activity Report (SAR), or even eventually replace it.

"When I talk to people about this case, I want others to know that understanding the data collected by peer-to-peer app companies or providers is important," he said. "Doesn't matter if they're a fintech company or tech company or whatever. This is how we're homing in and solving these crimes.

"There's a lot of companies that will store a lot, and some don't, and some don't know [what they have]. I really want to emphasize is that if everybody in law enforcement is able to learn how to identify these things and work collaboratively with people in the financial sector and have them be able to tell us, yes, we collect this or, no, we don't collect that, it can make our investigations run seamlessly."

What's in Store for the Future of Prepaid?

Industries are increasingly becoming consumer led rather than producer led, and prepaid is no exception.

"[The only thing keeping me up at night] is what can we do to best anticipate the needs of the consumer in the future, and not design ourselves into a hole?" Ault said. "We think we may have a great solution, we may think we can sell it, but is it something that's going to withstand the test of time?

"If it really, truly serves a consumer need, and has a beneficial impact for them, and we can tie it and layer it into other benefits, then I think that's the way to go."

Other themes coloring in the future of prepaid included an increased emphasis on liquidity and immediacy. The more prepaid card providers can remove friction from the ecosystem, the more appealing they will be to businesses and consumers alike.

As the payments landscape continues to shift, be it from innovation within or external forces such as regulations and economic necessity, where players can provide value can define their spot in this evolving financial ecosystem.

1Baig, A., Hall, B., Jenkins, P., Lamarre, E., & McCarthy, B. (2020, December 14). The COVID-19 recovery will be digital: A plan for the first 90 days.

2Kail, B., Masslive (2021, Mar. 21) "IRS Says Prepaid Debit Cards, More Paper Stimulus Checks Arriving This Week."

3Murphy, K. (2020, November 24). California inmates part of $1B unemployment fraud schemes, prosecutors say.